Chinese

Paperback

₹7052

(All inclusive*)

Delivery Options

Please enter pincode to check delivery time.

*COD & Shipping Charges may apply on certain items.

Review final details at checkout.

Looking to place a bulk order? SUBMIT DETAILS

Piracy-free

Assured Quality

Secure Transactions

About The Book

Description

Author

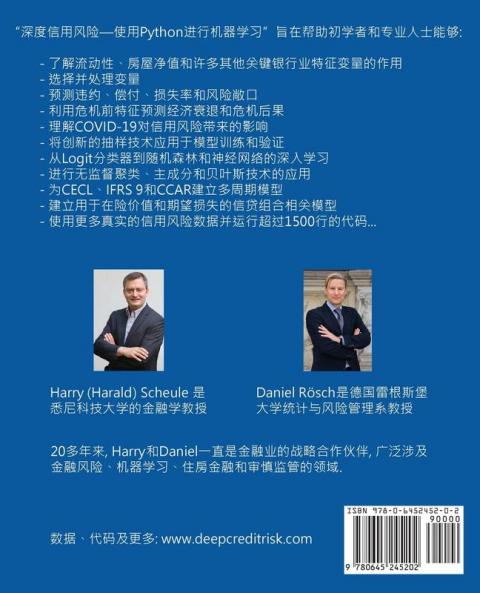

- 了解流动性,房屋净值和许多其他关键银行业特征变量的作用;- 选择并处理变量;- 预测违约、偿付、损失率和风险敞口;- 利用危机前特征预测经济衰退和危机后果;- 理解COVID-19对信用风险带来的影响;- 将创新的抽样技术应用于模型训练和验证;- 从Logit分类器到随机森林和神经网络的深入学习;- 进行无监督聚类、主成分和贝叶斯技术的应用;- 为CECL、IFRS 9和CCAR建立多周期模型;- 建立用于在险价值和期望损失的信贷组合相关模型;- 使用更多真实的信用风险数据并运行超过1500行的代码...- Understand the role of liquidity equity and many other key banking features- Engineer and select features- Predict defaults payoffs loss rates and exposures- Predict downturn and crisis outcomes using pre-crisis features- Understand the implications of COVID-19- Apply innovative sampling techniques for model training and validation- Deep-learn from Logit Classifiers to Random Forests and Neural Networks- Do unsupervised Clustering Principal Components and Bayesian Techniques- Build multi-period models for CECL IFRS 9 and CCAR- Build credit portfolio correlation models for VaR and Expected Shortfal- Run over 1500 lines of pandas statsmodels and scikit-learn Python code- Access real credit data and much more ...

Piracy-free

Assured Quality

Secure Transactions

Delivery Options

Please enter pincode to check delivery time.

*COD & Shipping Charges may apply on certain items.

Review final details at checkout.

Details

ISBN 13

9780645245202

Publication Date

-23-07-2021

Pages

-456

Weight

-791 grams

Dimensions

-191x235x23.41 mm