English

Hardback

₹10927

₹11100

1.56% OFF

(All inclusive*)

Delivery Options

Please enter pincode to check delivery time.

*COD & Shipping Charges may apply on certain items.

Review final details at checkout.

Looking to place a bulk order? SUBMIT DETAILS

Delivery Options

Please enter pincode to check delivery time.

*COD & Shipping Charges may apply on certain items.

Review final details at checkout.

About The Book

Description

Author

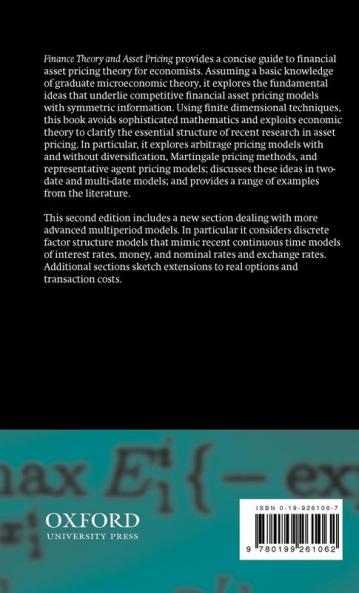

This text provides a concise guide to financial asset pricing theory for economists. Assuming a basic knowledge of graduate microeconomic theory it explores the fundamental ideas that underlie competitive financial asset pricing models with symmetric information. Using finite dimensional techniques the book avoids sophisticated mathematics and exploits economic theory to clarify the essential structure of recent research in asset pricing. In particular it explores arbitrage pricing models with and without diversification Martingale pricing methods and representative agent pricing models; discusses these ideas in two-date and multi-date models; and provides a range of examples from the literature. This second edition includes a new section dealing with more advanced multiperiod models. In particular it considers discrete factor structure models that mimic recent continuous time models of interest rates money and nominal rates and exchange rates. Additional sections sketch extensions to real options and transaction costs.

Piracy-free

Assured Quality

Secure Transactions

Fast Delivery

Sustainably Printed

Details

ISBN 13

9780199261062

Publication Date

-20-03-2003

Pages

-248

Weight

-373 grams

Dimensions

-140x216x17.46 mm