This Book is Out of Stock!

English

Hardback

₹7271

₹9482

23.32% OFF

(All inclusive*)

Delivery Options

*COD & Shipping Charges may apply on certain items.

Review final details at checkout.

Looking to place a bulk order? SUBMIT DETAILS

*COD & Shipping Charges may apply on certain items.

Review final details at checkout.

About The Book

Description

Author(s)

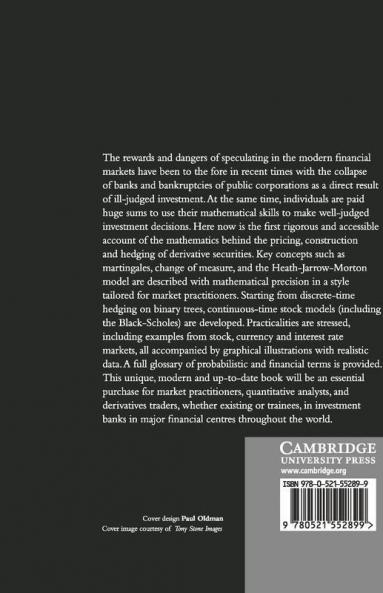

Here Is The First Rigorous And Accessible Account Of The Mathematics Behind The Pricing Construction And Hedging Of Derivative Securities. With Mathematical Precision And In A Style Tailored For Market Practioners The Authors Describe Key Concepts Such As Martingales Change Of Measure And The Heath-Jarrow-Morton Model. Starting From Discrete-Time Hedging On Binary Trees The Authors Develop Continuous-Time Stock Models (Including The Black-Scholes Method). They Stress Practicalities Including Examples From Stock Currency And Interest Rate Markets All Accompanied By Graphical Illustrations With Realistic Data. The Authors Provide A Full Glossary Of Probabilistic And Financial Terms.

Piracy-free

Assured Quality

Secure Transactions

₹7271

₹9482

23% OFF

Hardback

Out Of Stock

All inclusive*

Details

ISBN 13

9780521552899

Publication Date

-19-09-1996

Pages

-244

Weight

-424 grams

Dimensions

-151.89x228.09x14.54 mm