English

Paperback

₹5194

₹7804

33.44% OFF

(All inclusive*)

Delivery Options

Please enter pincode to check delivery time.

*COD & Shipping Charges may apply on certain items.

Review final details at checkout.

Looking to place a bulk order? SUBMIT DETAILS

Delivery Options

Please enter pincode to check delivery time.

*COD & Shipping Charges may apply on certain items.

Review final details at checkout.

About The Book

Description

Author(s)

Shoutouts

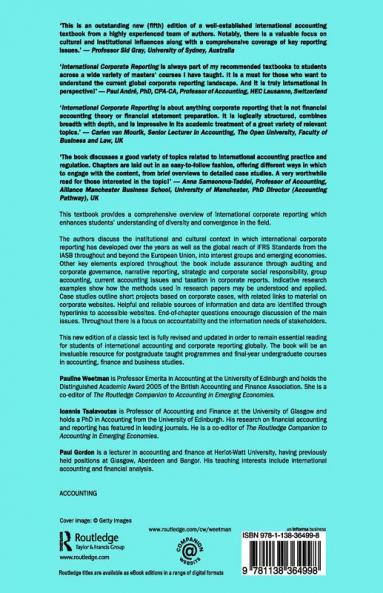

<p>This textbook provides a comprehensive overview of international corporate reporting which enhances students’ understanding of diversity and convergence in the field. </p><p>The authors discuss the institutional and cultural context in which international corporate reporting has developed over the years as well as the global reach of IFRS Standards from the IASB throughout and beyond the European Union into interest groups and emerging economies. Other key elements explored throughout the book include assurance through auditing and corporate governance narrative reporting strategic and corporate social responsibility group accounting current accounting issues and taxation in corporate reports. Indicative research examples show how the methods used in research papers may be understood and applied. Case studies outline short projects based on corporate cases with related links to material on corporate websites. Helpful and reliable sources of information and data are identified through hyperlinks to accessible websites. End-of-chapter questions encourage discussion of the main issues. Throughout there is a focus on accountability and the information needs of stakeholders.</p><p>This new edition of a classic text is fully revised and updated in order to remain essential reading for students of international accounting and corporate reporting globally. The book will be an invaluable resource for postgraduate taught programmes and final-year undergraduate courses in accounting finance and business studies. </p>

Piracy-free

Assured Quality

Secure Transactions

Fast Delivery

Sustainably Printed

Details

ISBN 13

9781138364998

Publication Date

-03-03-2020

Pages

-446

Weight

-881 grams

Dimensions

-174x246x23.68 mm

Imprint

-TAYLOR AND FRANCIS GROUP LIMITED